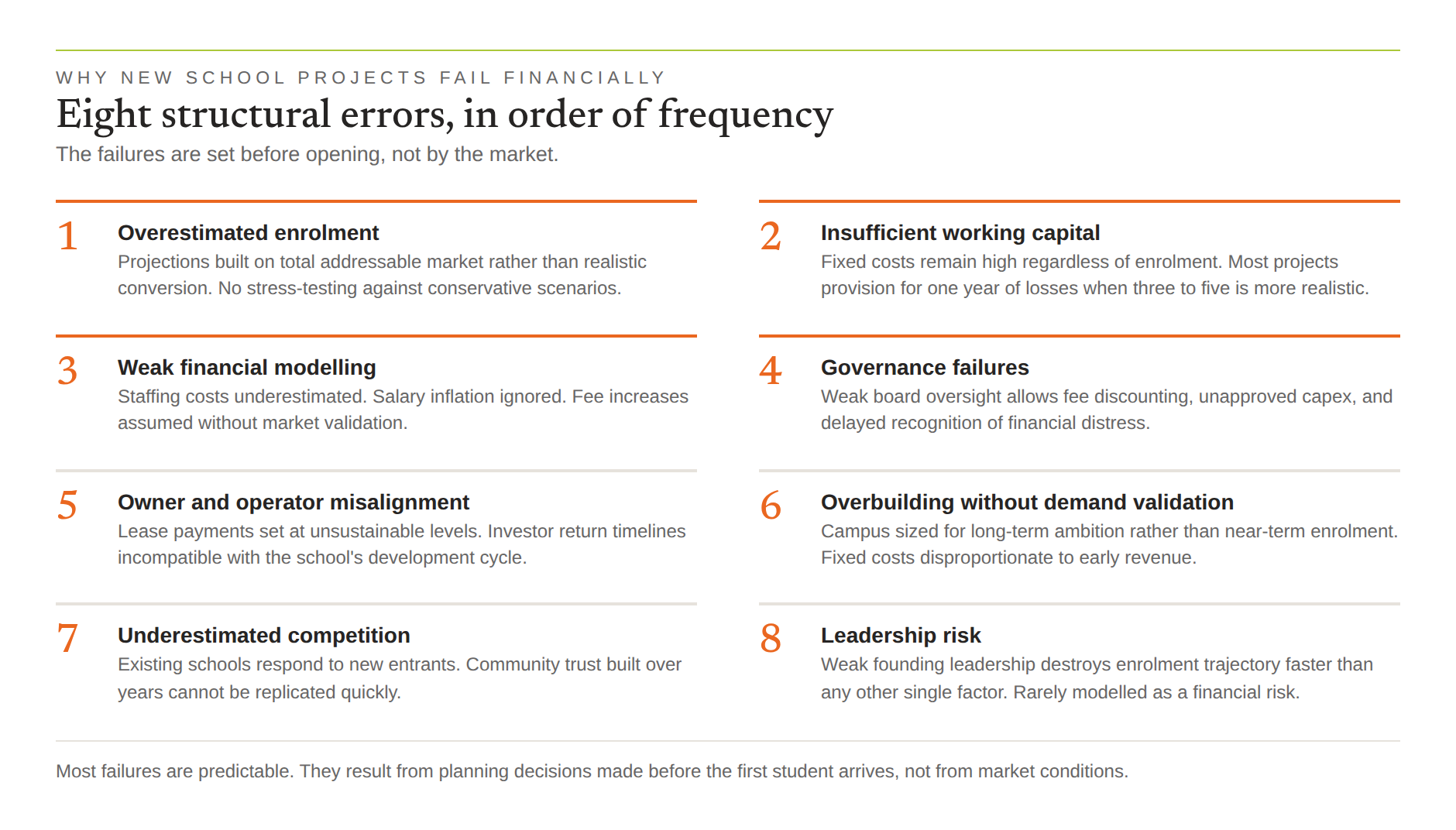

Education is widely regarded as a resilient, high-impact investment sector. Schools generate recurring revenue, serve essential community needs, and operate in markets where demand is often structurally undersupplied. Yet a significant proportion of new school projects struggle financially within their first five years, and some fail entirely.

The reasons rarely have anything to do with the quality of teaching or the strength of the educational vision. In almost every case, financial failure at a new school can be traced to a small number of structural planning errors made well before the first student arrived. Understanding those errors and why they are so consistently repeated is the most useful thing an investor or developer can do before committing capital to a new project.

The Enrolment Problem

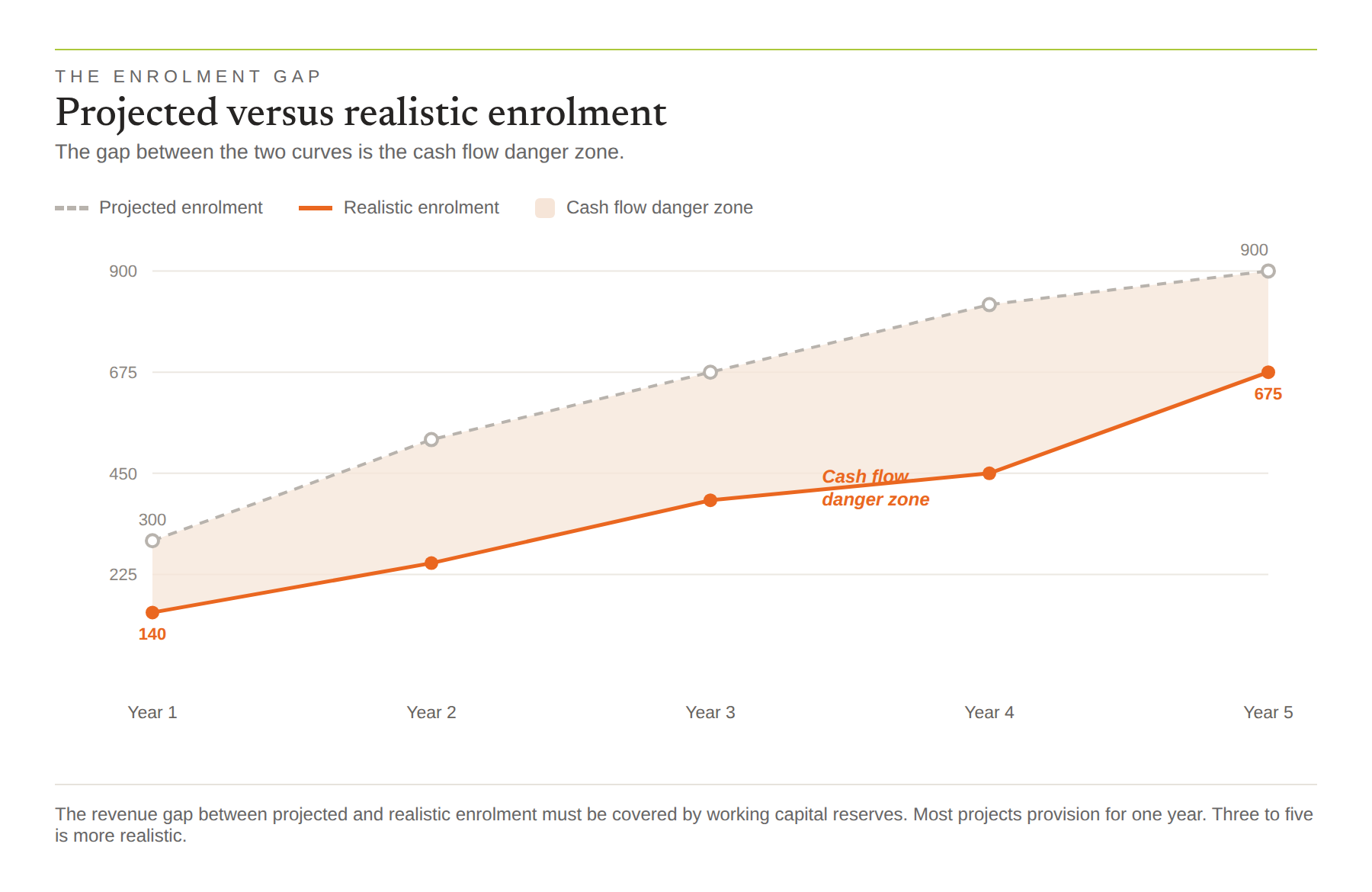

Overestimating enrolment is the single most common cause of financial failure in new schools and the most predictable. Developers and investors consistently build financial models on enrolment assumptions that are optimistic rather than evidence-based, and the consequences compound quickly.

The pattern is familiar. A new school opens, with projections showing 300 students in year one, growing to 600 by year three, and reaching full capacity of 900 by year five. The actual enrolment in year one is 140. By year three, it has reached 320. The gap between projected and actual revenue in years one through three is large enough to exhaust the working capital reserve, and the project enters financial distress before it has had a genuine opportunity to establish itself in the market.

The underlying cause is almost always the same. The enrolment projections were built on the total addressable market rather than on realistic conversion assumptions. They did not account for the time required to build community trust in a new institution. They did not model the competitive response from existing schools. And they were not stress-tested against a conservative scenario.

A thorough school feasibility study should produce enrolment projections that a sceptical institutional investor would find credible, not projections that make the financial model work. The difference between those two things is where most projects get into trouble.

Underestimating the Working Capital Requirement

The second most consistent cause of financial failure is insufficient working capital. This is closely related to the enrolment problem but distinct from it. Even projects with realistic enrolment projections regularly underestimate the operational capital required to sustain the school through its growth phase.

Schools have a cost structure that is largely fixed in the short term. Staff salaries, facilities costs, utilities, and regulatory compliance obligations do not scale down proportionally when enrolment falls short of projections. A school that budgeted for 300 students but is operating with 140, and still carries most of the same fixed cost base. The revenue shortfall flows directly to the operating deficit, and if the working capital reserve is insufficient to absorb that deficit across multiple years, the project is in trouble.

The working capital requirement for a new school is typically larger than developers expect and larger than most financial models allocate. A realistic model should provision for operating losses across at least three years, with sufficient reserve to absorb a scenario where enrolment growth is 30 to 40 per cent below the base case. Projects that provision for one year of losses and then assume the base case will materialise are systematically undercapitalised.

Weak Financial Modelling

Poor financial modelling is both a cause of failure in its own right and an amplifier of every other risk. When the financial model is built on unrealistic assumptions, it produces a false sense of confidence that leads to inadequate capitalisation, premature expenditure decisions, and delayed recognition of financial distress.

The most common modelling errors are underestimating staffing costs, ignoring salary inflation and annual increments, assuming fee increases without validating market tolerance, and failing to model the cash flow impact of delayed fee collection. Each of these would be manageable individually. In combination, they consistently produce financial models that overstate revenue and understate costs by enough to make a borderline project look viable and a genuinely viable project look spectacular.

The financial characteristics that determine whether a school project succeeds are the same ones that drive valuation in acquisition scenarios. Read our guide to how to value an international school.

Financial models for school projects should be built conservatively, stress-tested against multiple scenarios, and reviewed by someone with direct experience of school operating economics, not just general financial modelling experience. The specific cost dynamics of international schools, including expatriate staff packages, curriculum licensing fees, accreditation costs, and staffing ratios required by different curriculum frameworks, are not well understood outside the sector and are frequently underestimated by advisors without direct experience in the education sector.

The pattern of failure in PE-backed school groups follows a consistent logic, explored further in our article on private equity in education.

Governance Failures

The relationship between governance and financial performance in school projects is more direct than most developers recognise. Weak governance structures do not just create reputational or regulatory risk. They create financial risk, often at the worst possible time.

Schools with weak board oversight consistently make the same financial mistakes. They allow management to pursue enrolment growth through fee discounting that damages long-term revenue quality. They approve capital expenditure without adequate demand validation. They fail to identify cash flow deterioration early enough to intervene before the working capital reserve is depleted. And they lack the escalation mechanisms needed to hold management accountable when financial performance diverges from projections.

The governance failures that cause financial distress are almost always visible in the early stages of a project to anyone looking carefully. Boards without financial expertise, accountability frameworks without measurable KPIs, reporting structures that give management control over what the board sees, and ownership arrangements that are ambiguous about who has authority to make which decisions are all indicators of governance risk that will eventually translate into financial consequences.

Misalignment Between Owners and Operators

Many school projects involve multiple parties with different roles, different risk profiles, and different return expectations. Property developers, education operators, investors, and management organisations each bring different objectives to the table, and when those objectives are not clearly aligned from the outset, the resulting tension consistently damages financial performance.

The most common misalignment is between property owners and operating entities in a PropCo/OpCo structure. Lease payments set at a level that satisfies the PropCo’s return requirements but exceeds what the OpCo can sustainably pay through its growth phase create financial stress that neither party anticipated at the time of structuring. The OpCo diverts operational capital to service the lease, underinvests in marketing and admissions, and, as a result, grows more slowly. The slower growth makes the lease burden heavier in relative terms, and a cycle of financial deterioration begins.

Misalignment between investors and education operators is also common and similarly damaging. Investors with a real estate or private equity background frequently expect financial returns on a timeline that is incompatible with the educational development cycle of a new school. When those expectations are not explicitly managed at the outset, they create pressure on financial decisions, such as premature fee increases or cost reductions in academic staffing, that damage the school’s enrolment performance and long-term asset value.

Overbuilding Without Demand Validation

Capital expenditure discipline is consistently undervalued in school development. The impulse to build a campus that reflects the school’s long-term ambition rather than its near-term enrolment reality is understandable but financially dangerous.

A campus designed for 1,500 students that opens with 200 students carries a fixed cost structure disproportionate to its revenue base. Debt service, maintenance, utilities, and the staffing required to manage a large facility all consume capital that would otherwise be available to absorb the inevitable shortfalls of the early years. Phased development, where the campus is built incrementally as enrolment and revenue grow, is almost always the more financially sustainable approach.

The resistance to phased development typically comes from the belief that a premium facility is necessary to attract the enrolment needed to justify the investment. In competitive markets with established schools, this argument has some validity. But in most emerging markets, the quality of the academic programme and the reputation of the leadership team are far more influential drivers of enrolment than the size of the swimming pool or the sophistication of the performing arts centre.

Underestimating Competition

New school projects are frequently developed on the assumption that existing schools in the market are operating at or near capacity and that demand for additional places is straightforward to capture. That assumption is often wrong in ways that the financial model does not reflect.

Existing schools respond to new entrants. They improve their marketing, review their fee structures, invest in facility upgrades, and actively retain their families. The competitive response from established schools is one of the most consistently underestimated risks in new school development, and it directly affects the enrolment ramp that the financial model depends on.

Competitive analysis for a new school project should assess not just the current state of the market but the likely competitive response to a new entrant. Schools that have been operating in the market for a decade or more have established community relationships, brand recognition, and operational efficiency that a new school will take years to replicate. The new school’s differentiation must be genuine and compelling enough to attract families away from institutions they already trust.

The Leadership Risk

Financial models do not account for leadership quality, yet it is one of the most significant determinants of a new school’s financial performance. A founding principal who can build community confidence quickly, attract strong teaching staff, and establish an academic reputation that drives enrolment through word of mouth is worth more to the financial performance of a new school than almost any other single factor.

The inverse is equally true. A weak founding leadership team can destroy the enrolment trajectory of a technically well-structured project in a single academic year. Parent communities make decisions quickly and share experiences widely. A school that fails to establish credibility with its founding cohort of families faces an enrolment challenge that is extremely difficult to recover from.

Investors who take leadership quality as seriously as financial modelling, and who ensure that the management partner responsible for the school has the track record and the systems to find, appoint, and support the right founding leadership, consistently achieve better outcomes than those who treat leadership as an operational detail to be resolved after the capital is committed.

Building a More Resilient Project

The financial risks that cause school projects to fail are well understood and largely avoidable. They are not the product of bad luck or unpredictable market conditions. They are the product of planning decisions made early in the project lifecycle, when the pressure to demonstrate a compelling investment case can override the discipline needed to stress-test it honestly.

The projects that survive tend to do the dull things well: conservative enrolment numbers, enough working capital to absorb a slow start, honest financial models, and leadership hired with the same care as the capital is raised. None of it is hard on its own. Holding all of it together, under pressure to move fast, is the real test.

Global Services in Education (GSE) works with investors, developers, and school operators to design school projects that are structured to succeed from the outset. From feasibility and financial modelling through to ongoing school management, GSE brings the sector experience and investment discipline that serious education projects require, backed by 39 school projects delivered across 16 countries.

For more on investing in international schools, see our investment advisory and M&A work.