How to Value an International School

School valuation is one of the least understood areas of education investment. Investors who have bought and sold commercial property, manufacturing businesses, or technology companies often find that the frameworks they rely on in those sectors do not transfer cleanly to schools. The reasons are not complicated, but they matter enormously. A school’s value is not simply a function of its revenue and EBITDA. It reflects the quality of its educational programme, the strength of its community, the durability of its enrolment, its regulatory standing, and the degree to which its performance depends on individuals who may not stay. Getting this wrong in either direction, overpaying for a school that looks stronger than it is, or undervaluing one that the market has mispriced, is expensive.

This article covers the main valuation methodologies used in international school transactions, the factors that drive premium and discount pricing, and what buyers and sellers need to understand before engaging in a school acquisition or sale process.

Why School Valuation Is Different

Most business valuations rest on a relatively clean relationship between earnings and value. Apply a multiple to EBITDA, adjust for growth, debt, and risk, and you have a working estimate. Schools carry this logic but layer significant complexity on top of it.

The first layer is community dependency. A school’s enrolment is not a customer list. It is a community of families who chose the school for specific reasons, including curriculum, culture, leadership, and peer group. If any of those change materially post-acquisition, families leave. An enrolment base that looks stable in the data room can erode quickly if the buyer mismanages the transition. Acquirers who have treated school enrolment like a subscription revenue base, assuming high retention regardless of what happens operationally, have consistently been surprised.

The second layer is the relationship between quality and value. In most businesses, cutting costs improves margin and therefore value. In schools, cutting costs in the wrong places, removing experienced teachers, reducing curriculum resources, or allowing facilities to deteriorate, damages the educational reputation that the enrolment depends on. Value in schools is preserved by maintaining quality, not by extracting from it.

The third layer is regulatory exposure. International schools operate under licences that can be withdrawn, conditions that must be met, and fee frameworks that constrain revenue growth in some markets. A school’s regulatory standing is a material component of its value and needs to be assessed with the same rigour as its financial statements.

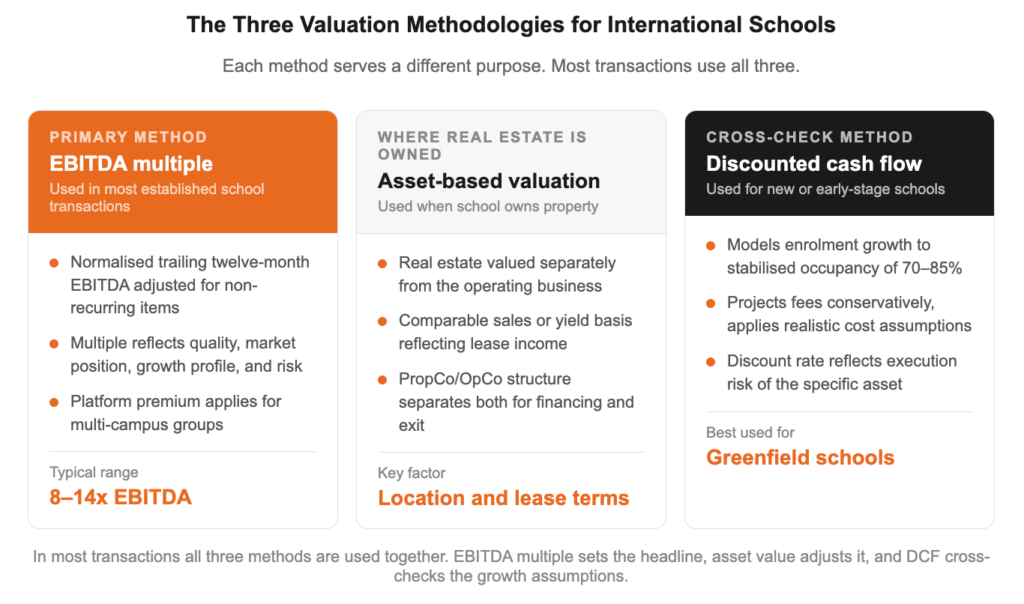

The Three Main Valuation Methodologies

EBITDA multiple

The most common methodology for international school transactions is the EBITDA multiple. A normalised EBITDA figure, typically based on the trailing twelve months adjusted for non-recurring items and owner-specific costs, is multiplied by a factor that reflects the school’s quality, market position, growth profile, and risk characteristics.

Multiples in the international school sector have historically ranged from 8 to 14 times EBITDA for established schools with strong enrolment and credible management. CIS-accredited schools in supply-constrained markets with a demonstrated track record of enrolment growth command the upper end. Schools with enrolment concentration risk, regulatory uncertainty, or leadership dependency trade at a discount.

For school groups operating multiple campuses, a platform premium applies. A group of five schools is worth more than five times a single school because of the economies of scale, the diversification of risk across sites, and the strategic optionality it provides to acquirers looking to expand further.

Asset-based valuation

Where a school owns its real estate, the asset base contributes directly to value and needs to be assessed separately from the operating business. The PropCo/OpCo structure that has become standard in international school transactions exists precisely to allow real estate value and operating business value to be recognised and financed independently.

The real estate component is typically valued on a comparable sales basis or on a yield basis reflecting the lease income it generates from the operating entity. School real estate in good locations with long lease terms commands a yield premium over general commercial property because of its essential-service characteristics and the stability of its income.

For schools operating on leased premises, the asset-based component is less significant, and the valuation is more purely a function of operating earnings.

Discounted cash flow

DCF analysis is used as a cross-check in most school transactions rather than as the primary valuation methodology. It is particularly useful for greenfield or early-stage schools where there is limited earnings history but a credible enrolment trajectory and a clear path to mature EBITDA margins.

A DCF for a new school typically models enrolment growth from opening to a stabilised occupancy of 70 to 85 percent of capacity, projects fees on a conservative basis, applies realistic operating cost assumptions, and discounts the resulting cash flows at a rate that reflects the execution risk of a pre-operating or early-stage asset. The discount rate applied to a new school in a proven market with a strong local partner will differ materially from one applied to a new school in an untested location with an inexperienced operator.

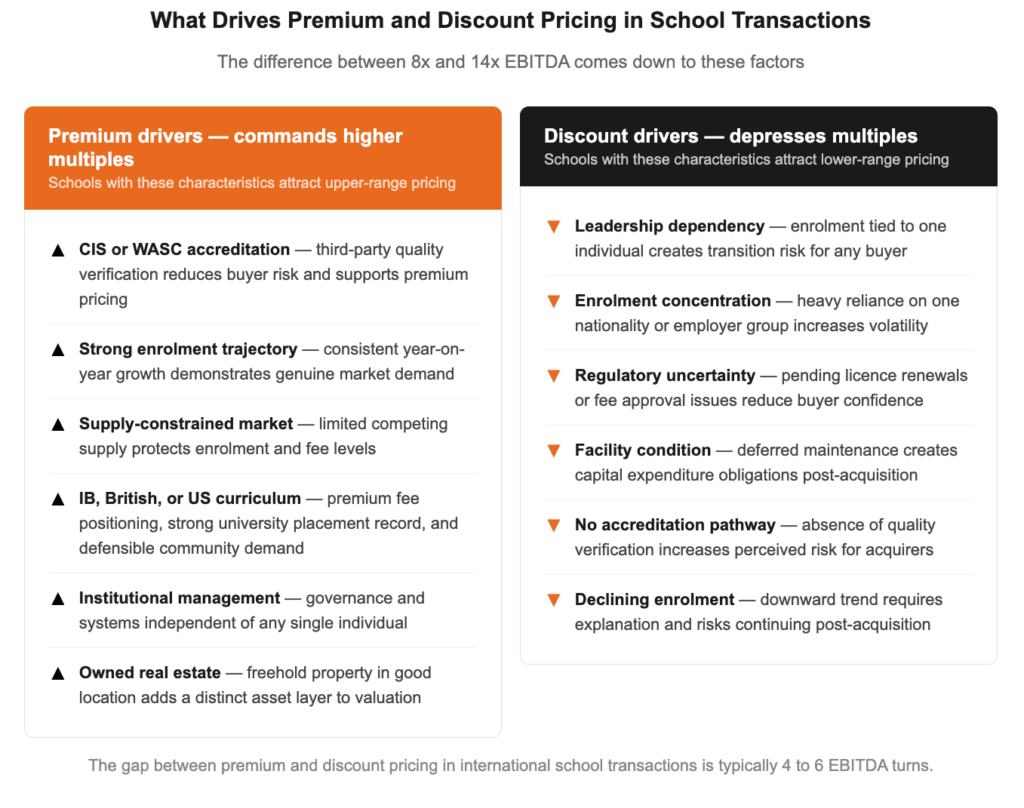

What Drives Premium Valuation

Understanding what drives premium pricing in school transactions is as important as understanding the methodology. Buyers pay more for schools that demonstrate the following characteristics.

Enrolment depth and durability. A school with a long waitlist, high sibling enrolment rates, and a history of consistent growth across economic cycles is worth significantly more than one dependent on annual re-enrolment campaigns. Enrolment durability is the single most important value driver in international schools because it underpins every other financial metric.

Curriculum strength and accreditation. Schools with credible international accreditation from bodies such as CIS or WASC, or with IB authorisation, command a premium over comparable unaccredited schools. The full breakdown of how each accreditation body works, what the process involves, and which one fits which market is covered in our article on how to get international school accreditation. US curriculum schools authorised by Cognia or accredited through WASC carry similar weight with American university admissions offices and with the significant US expatriate and internationally mobile communities they serve, which adds a distinct and defensible enrolment base that acquirers value. Accreditation is third-party verification of quality that reduces the due diligence burden for acquirers and provides assurance to the parent community post-transaction.

Fee positioning and pricing power. A school operating at a fee level below what its quality and market position would support is an opportunity for a buyer who can close that gap. A school already at the ceiling of its market’s fee tolerance has less upside. Understanding where a school sits relative to the competitive fee band in its specific market is essential to assessing its revenue growth potential. US curriculum schools typically occupy a distinct fee band from IB and British curriculum schools in the same market, reflecting the size and spending power of the American and internationally mobile community they serve. In markets like Dubai, Singapore, and the GCC, this positioning creates a defensible niche with strong renewal characteristics.

Management quality and transferability. If a school’s performance is heavily dependent on a single principal or founder, the risk of value erosion post-transaction is significant. Buyers pay more for schools with institutional strength, distributed leadership, documented systems, and a culture that does not depend on any one individual to function. This is one of the reasons why governance structures are a material component of school valuation rather than a peripheral consideration.

Regulatory standing. A school with a clean regulatory record, current licences, and a strong relationship with its host country education authority is worth more than one with outstanding compliance issues or a history of regulatory friction. In markets like the GCC, where licensing processes are substantive and relationships matter, regulatory standing is a genuine value differentiator.

Facility quality. Schools with modern, well-maintained facilities appropriate to their curriculum and fee level are worth more than those with deferred maintenance or ageing infrastructure. Facility quality affects both enrolment competitiveness and the capital expenditure burden facing the acquirer post-transaction.

What Drives Discount Valuation

The same logic applies in reverse. Schools trade at a discount when they carry identifiable risks that a buyer must either accept or price out.

Enrolment concentration in a single nationality or expatriate community creates dependency on labour market flows that can reverse quickly. US curriculum schools should be assessed carefully on this dimension. A school whose enrolment is drawn primarily from US government, military, or corporate postings is more exposed to policy-driven relocation than one serving a broader American and internationally mobile community. A school whose enrolment is 70 percent dependent on one corporate employer’s staff is significantly more vulnerable than one serving a diversified community.

Leadership dependency, as described above, is a consistent discount factor. A principal who has built the school over fifteen years and whose departure would trigger significant parent anxiety deserves careful scrutiny in any due diligence process.

Fee suppression in regulated markets, particularly in Saudi Arabia under the Tadarruj framework, can constrain revenue growth regardless of the quality of the school. Buyers need to understand the approved fee trajectory and the realistic path to fee improvement before applying a growth multiple.

Deferred capital expenditure that has been masked in the accounts creates a hidden liability. A school that looks profitable but requires significant facility investment to remain competitive is worth less than its headline EBITDA suggests.

The Due Diligence Process

A credible school valuation requires due diligence that goes beyond the financial statements. Many of the risks that show up in a poorly executed due diligence process are the same structural weaknesses that cause school projects to fail financially in the first three to five years of operation. The following areas require specific attention.

Enrolment data should be examined over a minimum of five years, broken down by year group, nationality, and payment record. Re-enrolment rates, waitlist depth, and sibling enrolment ratios are more informative than headline student numbers.

Regulatory documentation should be reviewed in full, including the current licence, any conditions attached to it, correspondence with the host country education authority, and the school’s inspection or audit history.

Staff data should cover teacher turnover rates, the proportion of staff on local versus international contracts, and the school’s record of renewing key personnel. High turnover in teaching staff is a leading indicator of cultural or operational problems that will not be visible in the financial accounts.

Parent satisfaction data, where available through formal surveys or inspection reports, provides an independent view of the school’s community standing that complements the financial picture.

Competitor analysis should assess the school’s position relative to other providers in its catchment area, including any new schools under development that could affect demand.

The Role of an Experienced Operator in Valuation

A school’s value to a particular buyer depends partly on that buyer’s ability to operate it well. An experienced education operator acquiring a school that is underperforming relative to its potential will generate better returns than a financial buyer acquiring the same asset without the operational capability to improve it.

This is why the combination of financial expertise and educational operational knowledge is important in school acquisitions. GSE works with investors across the full transaction lifecycle, from pre-acquisition market and feasibility assessment through to post-acquisition management and school improvement. Understanding what a school is worth today and what it could be worth under experienced management are two different questions, and the gap between the answers is often where the investment case lies.

For buyers and sellers considering a school transaction, a conversation with GSE at the earliest stage of the process is the most efficient way to ensure that valuation assumptions are grounded in operational reality rather than financial modelling alone.

Contact GSE to discuss your school acquisition or valuation requirements.

Related Articles

- Private Equity in Education: What Investors Need to Know

- EBITDA Benchmarks: How Profitable Are International Schools?

- The PropCo/OpCo Model in School Development Explained

- School Governance Structures That Attract Education Investors

- How to Get International School Accreditation

- Why Most New School Projects Fail Financially

- How to Conduct a Feasibility Study for a New School

- The Valuation Process for a School Investment

- International School Development

- Contact GSE

There must be a clear strategy and plan to make a school project investment ready: Learn more

👉 [10 Steps to Setting Up a New School]

Meet Our Founder and CEO

Greg Parry

Greg Parry is the founder and CEO of Global Services in Education. GSE has delivered school development and management projects across more than 35 countries, working with investors, developers, governments and operators from feasibility through to opening and beyond. Greg advises on the commercial decisions that determine whether a school project succeeds: deal structure, financial viability, governance, and the operating model that carries the school once it opens.

His work spans the GCC, Southeast Asia, Europe and Africa, and the focus throughout is practical. Schools that are built to perform, and projects that are structured to last.

📩 Contact Greg Parry Directly [Contact Link]

GSE’s Comprehensive School and University Development Services

GSE offers end-to-end solutions tailored for new and existing schools, covering:

School Management & Operations

Strategic Planning & Feasibility Studies, including Financial modelling

Architectural & Interior Conceptual Design

School Resources & ICT Planning

Marketing, Branding & Admissions

Staffing, Recruitment & Training

Curriculum Design & Accreditation Support

School Audits & Action Plans

Let’s Build a World-Class School Together!

Ready to start or improve your school?

Visit www.gsineducation.com

Recent Comments