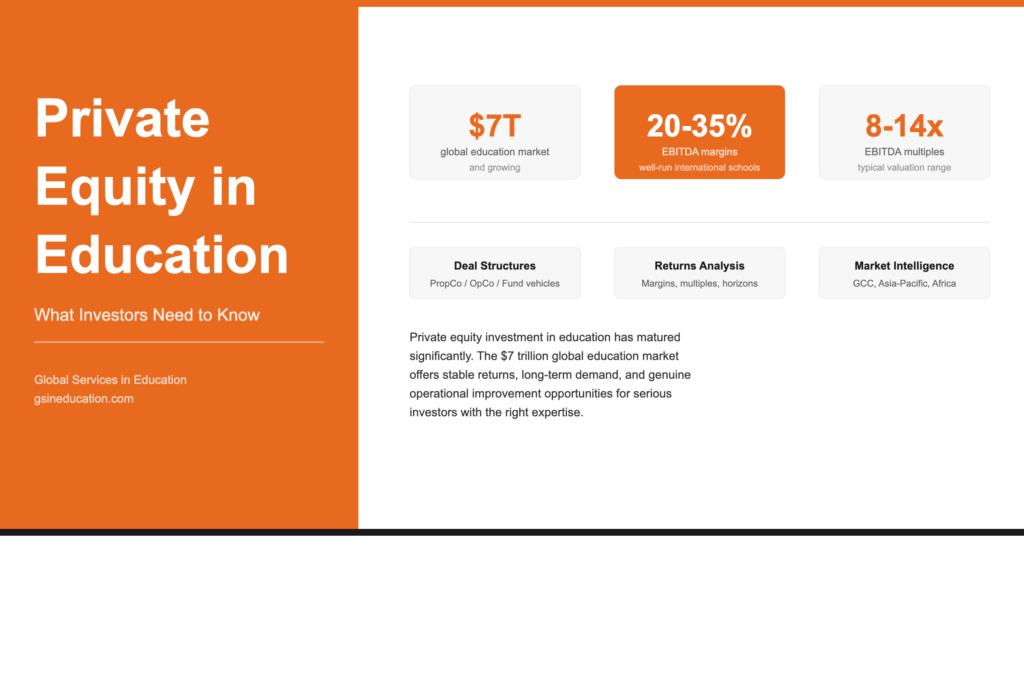

Private Equity in Education: What Investors Need to Know

Private equity’s relationship with the education sector has matured considerably over the past decade. What was once treated as a niche, mission-driven space, too complex, too regulated, and too reputationally sensitive for mainstream institutional capital, is now one of the most actively pursued sectors in the global private equity landscape. The global education market is valued at approximately $7 trillion and growing. Deal activity, while it corrected after the 2021 peak, has stabilised into a disciplined, outcomes-focused investment approach that is attracting serious capital from family offices, sovereign wealth funds, and PE firms with genuine sector expertise.

This article explains what private equity investment in education actually looks like, which segments attract the most capital, what returns are realistic, and what investors need to understand before committing to an education asset.

Why Education Attracts Private Equity Capital

The structural case for investment in education is well established. Demand is driven by demographics, not discretionary spending. Families continue to prioritise education during economic downturns, making the sector genuinely countercyclical in a way few other asset classes can credibly claim. Revenue is recurring. Tuition fees are paid annually, often in advance, across multi-year enrolment periods. The customer relationship is long-term, often spanning 12 or more years as families progress through school from early childhood to graduation.

For private equity specifically, education offers several characteristics that align with the asset class’s return-generation process. There are genuine operational improvement opportunities. Many school groups are underleveraged on management systems, curriculum positioning, facility utilisation, and cost structure. There are consolidation opportunities, particularly in fragmented emerging markets where independent school operators lack the capital to scale. And there are multiple exit pathways, including strategic acquirers, secondary PE transactions, and increasingly, listed vehicles and REIT-adjacent structures.

The international schools segment within private education is particularly attractive because it combines the structural demand characteristics of domestic private education with the geographic growth potential of emerging markets. International school enrolment has grown consistently across the GCC, Southeast Asia, Africa, and South Asia, driven by rising local demand from aspirational middle-class families rather than, as was historically the case, expatriate populations alone.

Where Private Equity Capital Is Going

Private equity activity in education spans several sub-sectors. Understanding which segments attract capital and why is essential for investors positioning themselves in the market.

International K-12 schools represent the largest and most established segment for private equity in education. The landmark transactions, including KKR’s investment in Cognita, BPEA EQT’s $4.3 billion take-private of Nord Anglia in partnership with CPPIB, and OMERS Private Equity’s investment in International Schools Partnership alongside Partners Group, have validated the sector at an institutional scale. These transactions are characterised by platform acquisition followed by bolt-on growth across geographies. The investment thesis is straightforward: acquire a quality operator with a proven curriculum and management model, apply capital to geographic expansion and facility improvement, and generate returns through enrolment growth, fee expansion, and EBITDA margin improvement.

Early childhood education has attracted significant PE interest in markets where the regulatory environment permits private provision and where supply remains constrained relative to demand. The unit economics of early childhood education differ materially from K-12. Lower capital requirements per seat, higher student-to-staff ratios, and faster ramp-up periods make it attractive for investors focused on near-term cash generation rather than long-duration assets.

EdTech dominated PE and venture capital activity between 2020 and 2022 during the pandemic-driven digitalisation surge, with deal volumes peaking at 110 transactions worth $4.2 billion in 2021. The subsequent correction has been significant. Deal volume fell to approximately 40 transactions by 2024. The market has moved from speculative growth toward backing platforms that integrate with traditional schools to improve outcomes and reduce operational costs. The pure-play digital school model has largely failed to deliver at scale.

Vocational and higher education remain active segments, particularly in markets where government-funded provision is undersupplied or where employer demand for specific skills is creating structural gaps that private providers can fill efficiently.

The International Schools Investment Case in Detail

For investors specifically considering private and international school assets, the financial characteristics are worth understanding in detail.

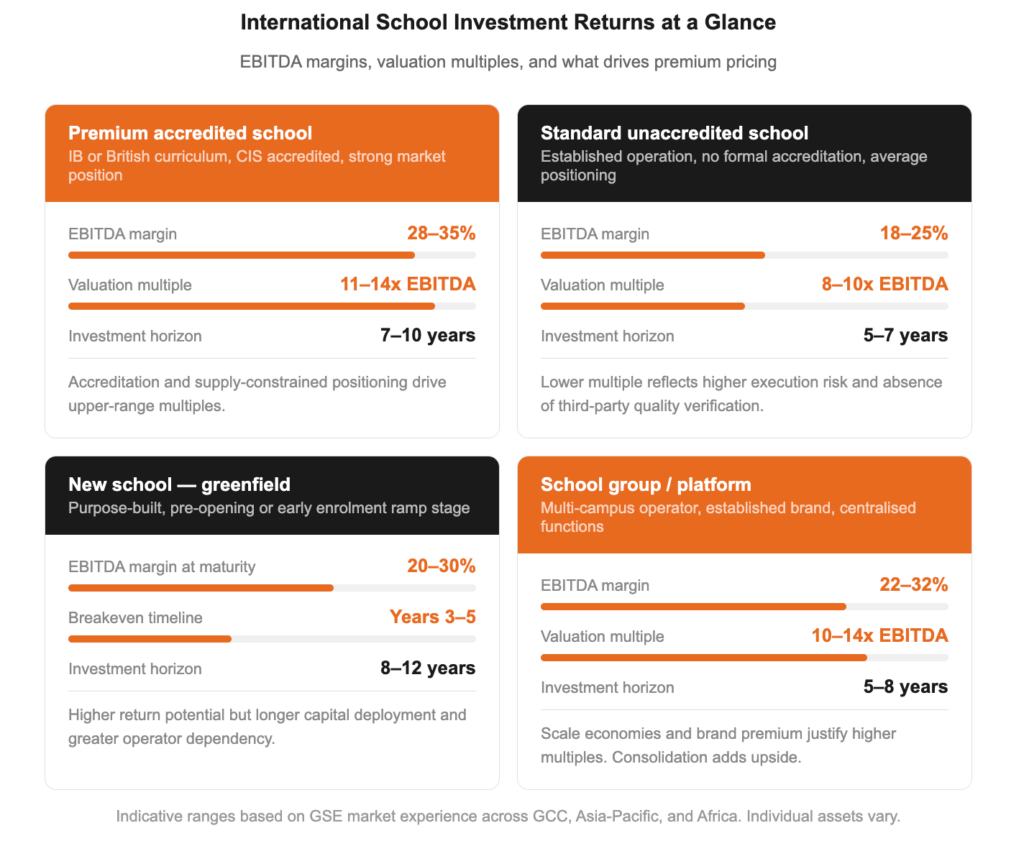

EBITDA margins in well-run international schools typically range between 20 and 35 per cent at the school level, with group-level margins depending heavily on the cost structure of central functions and debt servicing. Our EBITDA benchmarks article covers the financial performance data in detail. Fee elasticity varies significantly by market and curriculum positioning. An IB school in Dubai or Singapore operates in a fundamentally different pricing environment from a British-curriculum school in a secondary city in Southeast Asia.

Valuation multiples in the sector have historically ranged from 8 to 14 times EBITDA for individual schools and established groups, with premium assets in supply-constrained markets and strong curriculum positioning commanding the upper end of that range. For a detailed breakdown of how international schools are valued across different asset types and markets, read our guide to how to value an international school. CIS-accredited schools with demonstrated student outcomes and strong parent satisfaction scores consistently command higher multiples than comparable schools without accreditation. This is one of the reasons why accreditation planning should be embedded in the investment thesis from the outset rather than treated as an operational afterthought.

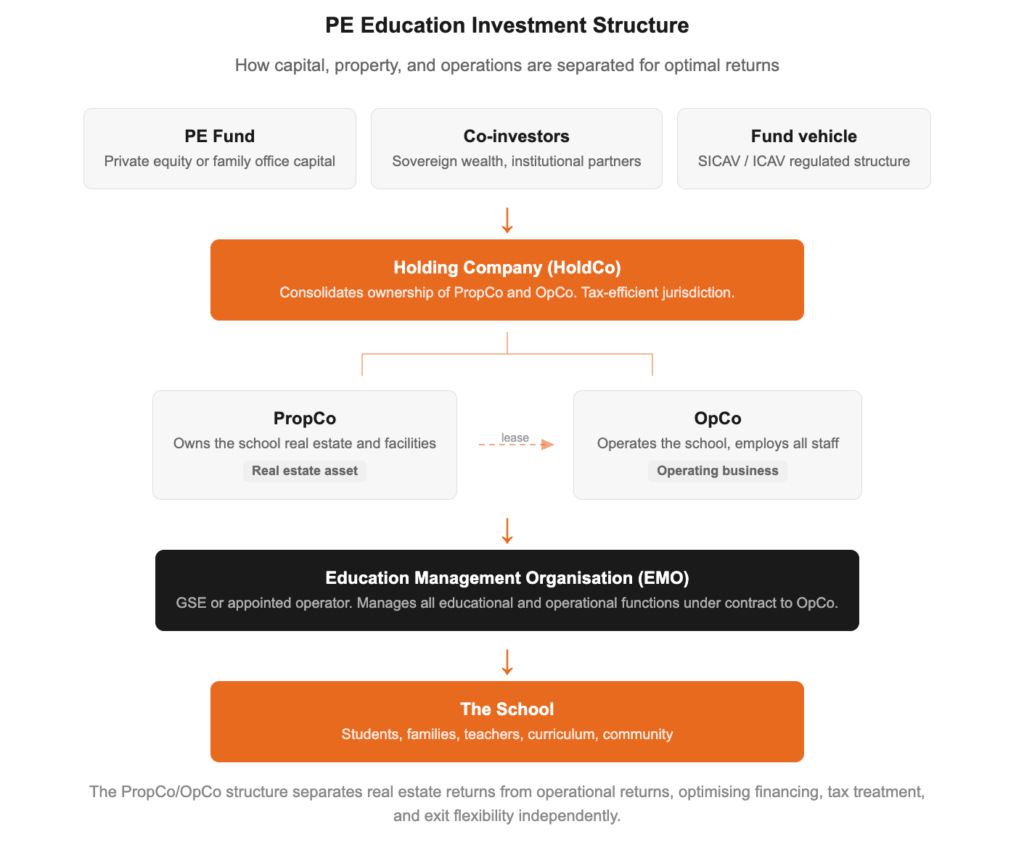

The PropCo/OpCo structure has become the dominant deal architecture for international school private equity, separating the real estate asset from the operating business to optimise financing, tax treatment, and exit flexibility. Understanding how this structure affects lease obligations, covenant setting, and the relationship between the two entities is essential for investors structuring new school projects or acquiring existing ones.

What Private Equity Gets Wrong in Education

The education sector has also produced its share of cautionary tales, and the pattern of failure is consistent enough to be instructive.

The most common error is treating education assets like conventional commercial property or consumer services businesses. Schools are community institutions. Parent satisfaction, teacher quality, curriculum integrity, and regulatory relationships are not variables that can be optimised away in pursuit of margin improvement without consequences. PE-backed school groups that have prioritised short-term financial performance over educational quality have consistently experienced enrolment declines, regulatory pressure, and reputational damage that have proved difficult to reverse. The structural reasons behind this are covered in detail in our article on why most new school projects fail financially.

The second common error is underestimating the regulatory complexity of operating across multiple jurisdictions. Licensing requirements, curriculum approval processes, fee regulations, and ownership restrictions vary enormously across markets. A model that works in Dubai does not translate directly to Saudi Arabia, nor to Malaysia or Kenya. Investors who enter markets without specialist knowledge of the regulatory environment consistently encounter delays, cost overruns, and compliance issues that erode returns.

The third error is acquiring or building schools without the management depth to operate them. Capital is necessary but not sufficient. The quality of the educational leadership team, the curriculum framework, the school culture, and the community relationships determine whether a school succeeds or fails in its market. PE investors who treat these as operational details to be addressed post-acquisition rather than as investment criteria applied at the acquisition stage consistently underperform.

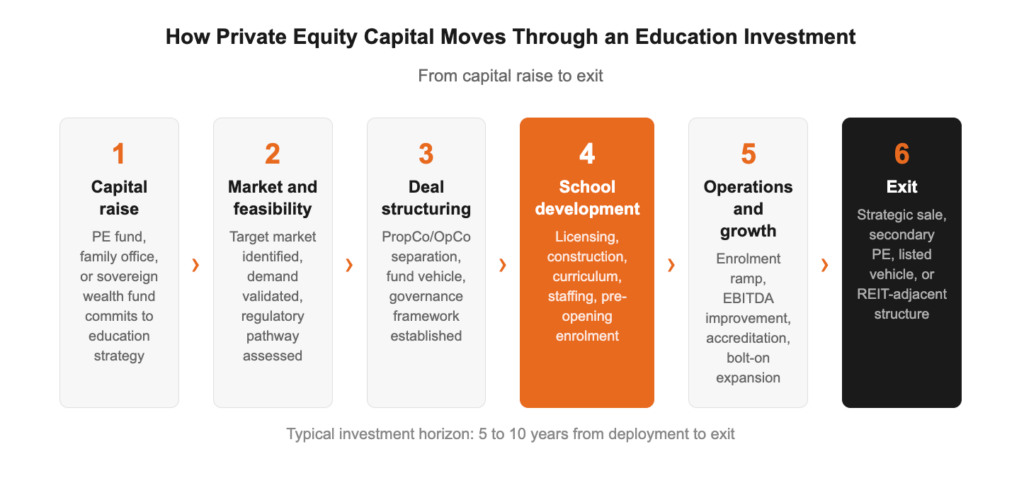

Deal Structures and Fund Vehicles

Private equity investment in education takes several structural forms that investors should understand.

Direct investment in individual schools or school groups through standard PE fund structures remains the most common approach. Co-investment alongside specialist fund managers is increasingly common as the sector attracts larger institutional participants seeking exposure to education without building dedicated sector expertise internally.

Regulated investment fund structures, including SICAVs based in Malta and ICAVs structured in Ireland, are increasingly used for education investment platforms seeking to aggregate capital from multiple investors across jurisdictions. These structures offer flexibility in sub-fund architecture, allowing education real estate and operating businesses to be held within the same regulated vehicle, with appropriate structural separation.

REIT-adjacent models, in which school real estate is aggregated into a property vehicle that generates lease income from operators, are gaining traction in markets where the real estate characteristics of school assets, including long leases, essential-service use, and predictable income, are recognised as distinct from those of general commercial property.

What Serious Investors Do Differently

The investors who have generated consistent returns in education share several characteristics that distinguish them from those who have not.

They engage specialist operators from the outset rather than attempting to apply generic operational improvement playbooks to institutions they do not understand. They build accreditation and regulatory compliance into the investment thesis and timeline rather than treating them as post-acquisition tasks. They structure their governance frameworks to preserve the educational culture and community trust that drive enrolment, rather than subordinating these to financial metrics. And they take a long-term view. The strongest returns in international school investment have come from patient capital with five to ten-year horizons, not from operators seeking quick exits.

GSE works with private equity investors, family offices, and sovereign wealth funds across the full education investment lifecycle, from feasibility and market analysis through to school development, management, and portfolio optimisation. Our advisory work spans the GCC, Southeast Asia, Africa, Europe, and beyond.

If you are exploring education as an asset class or assessing a specific school investment opportunity, we welcome an initial conversation. Contact GSE.

Related Articles

- Why Education Is the Next Frontier for Private Equity

- EBITDA Benchmarks: How Profitable Are International Schools?

- The PropCo/OpCo Model in School Development Explained

- School Governance Structures That Attract Education Investors

- How to Get International School Accreditation

- Why Most New School Projects Fail Financially

- How to Conduct a Feasibility Study for a New School

- International School Development

- Contact GSE

There must be a clear strategy and plan to make a school project investment ready: Learn more

👉 [10 Steps to Setting Up a New School]

Meet Our CEO & Education Expert

Greg Parry – International School Leadership Authority

Greg Parry is an international education investor and leadership consultant. He is the Co-Founder and CEO of Global Services in Education and GSE Capital Advisory Group, advising on school development, management, and education-focused investment worldwide. His work bridges leadership theory and practical transformation across more than thirty-five countries.

Greg Parry is a renowned global expert in education leadership, having led projects in Australia, the Middle East, the United States, India, Indonesia, Malaysia, and China. His accolades include:

🏆 Minister’s Award for Excellence in School Leadership

🏆 School of Excellence Award for Industry/School Partnerships

🏆 School of Excellence Award for Technology Innovation

🏆 Recognised for Best Global Brand in International Education (2015 & 2016)

With a strong track record in school start-up projects, leadership training, and curriculum development, Greg is a trusted authority in building and managing high-performing international schools.

📩 Contact Greg Parry Directly [Contact Link]

GSE’s Comprehensive School and University Development Services

GSE offers end-to-end solutions tailored for new and existing schools, covering:

✔ School Management & Operations

✔ Strategic Planning & Feasibility Studies, including Financial modelling

✔ Architectural & Interior Conceptual Design

✔ School Resources & ICT Planning

✔ Marketing, Branding & Admissions

✔ Staffing, Recruitment & Training

✔ Curriculum Design & Accreditation Support

✔ School Audits & Action Plans

Let’s Build a World-Class School Together!

💡 Ready to start or improve your school?

Visit www.gsineducation.com

Recent Comments